WHY SOUTH AFRICAN RETIREMENT FUNDS SHOULD ALLOCATE TO PRIVATE EQUITY

This article is the last in a series of seven exploring private equity investment, and serves as a summary / conclusion.

The global trend towards alternative asset classes, and private equity in particular, is unquestionable. However, South Africa has lagged behind. The good news though, is that we still have those levers to pull in order to enhance portfolio returns for members of retirement funds.

As with most trends, it is easiest to climb in last – when everyone else is already there. However, that is the least beneficial time to join a trend given that it signals the end of the trend. This trend towards private equity is not a matter of timing the market through cycles, but rather identifying a new pocket and making appropriate use of it. Those readers who were around when inflation-linked bonds were introduced in South Africa for the first time will recall those bonds producing guaranteed yields of 5% above inflation. That was a no-brainer to invest in, but demand has driven those rates closer to 2% above inflation. It was simply a new pocket of assets, with low demand as a result, which now reflects normalised demand.

It is reasonable to assume that the same pattern may be observed in private equity – the later you allocate capital towards the asset class, the lower the expected returns. The investment case is likely to continue to make sense at that point – perhaps just less so than now.

In this series of articles we have shared how retirement funds that would like to invest in a representative sample of companies in their economy, would need to shift some capital to private markets due to the number of companies that have shifted capital raising efforts there. If trustees would like to make up for the current lower returns environment, they will have to consider shifting even more exposure to private markets.

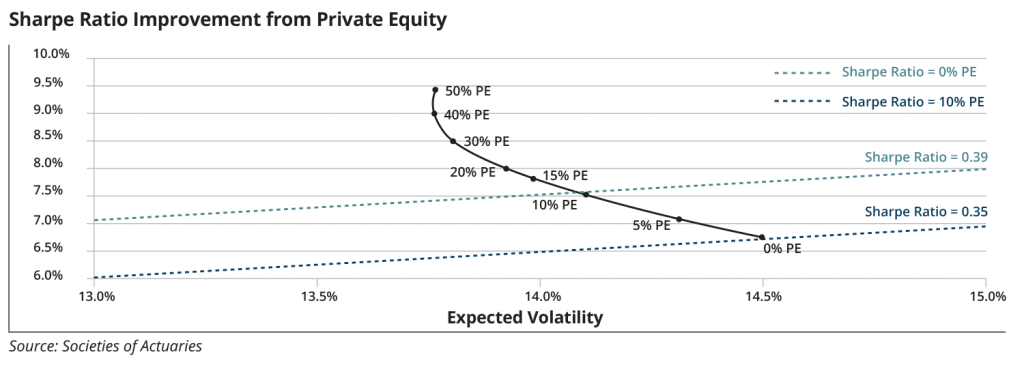

The Societies of Actuaries illustrated the expected return benefit of incorporating private equity into a portfolio construction process. Although this reduction in volatility is not a fair measure of risk, it does signify a real experience of less volatile returns for members.

Although Regulation 28 will not allow retirement funds to invest more than 10% in private equity, a 10% allocation already shows a meaningful change to a portfolio’s expected return and risk characteristics.

Even investing into private equity through a listed company in the UK has shown an average correlation with the general listed market of 0.3 (the highest was 0.5) due to investment into different segments of the economy, as well as different structures.

It is not often that an investor is able to increase expected returns and reduce expected volatility at the same time, and both at a substantial margin. Add to this benefit the social impact explored in this article and it does seem as though at least some investment in private equity is a “no-brainer”.

Empirically, there are substantial social and responsible investment benefits to allocating capital to private equity, including making companies better corporate citizens, better businesses, more efficiently run, as well as increasing employment levels and improving B-BBEE scores.

Although there are challenges to investing in private equity, appropriately structured funds of funds can address most – if not all – of them and make investment palatable and attractive for individuals and retirement funds alike.

Global investors are shifting their focus to emerging markets (Asia, South America and Sub-Saharan Africa), based on the clear trend of increasing GDP growth in the region. It would be sad if South African retirement funds remain the ones losing out relative to global investors, by allowing the latter to continue to benefit from private equity returns at the expense of members of local retirement funds.

It is worth repeating the warning of the head of investments at CalPERS (California Public Employees Retirement System – one of the biggest global retirement funds), Yu Ben Meng, who considers the current 8% allocation to private equity sub-optimal and wants to increase it to 16%.

Willem le Roux

Principal Investment Consultant and Actuary