2 of 2020

FSCA Communication 9 of 2020 – Impact of Covid-19 on compliance with various regulatory requirements and FSCA General Notice 2 of 2020 – Extension of period for compliance with various requirements related to the submission of statutory returns.

The Communication was issued on 26 March 2020 and deals with the impact of Covid-19 on compliance with various regulatory requirements. The FSCA sets out the various arrangements in respect of the submission of statutory returns and fit and proper related deadlines.

The FSCA also states that it will do its best to accommodate anyone who is experiencing problems in complying with regulatory requirements as a result of the impact of Covid-19.

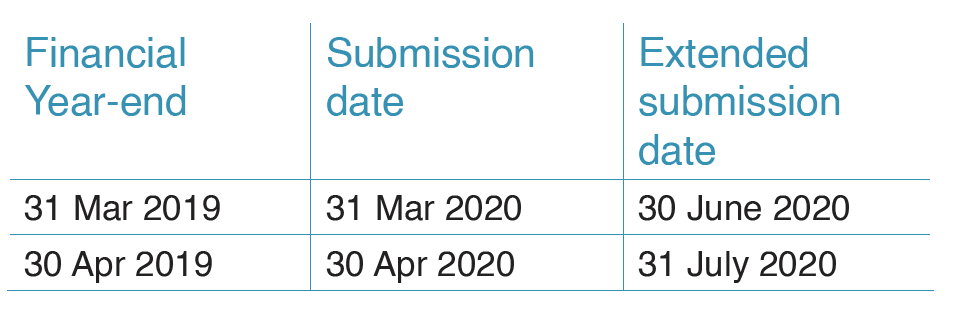

In the Communication, the FSCA extends the period for submission of financial statements by pension funds by three months and the extension is irrespective of any extensions that were already granted.

The extended submission dates are as follows:

The period for submission of valuation reports by pension funds is also extended by three months.

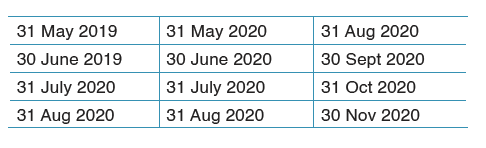

In the FSCA General Notice 2 of 2020 the extended submission dates are set out as follows:

FSCA Communication 11 of 2020 – Covid-19: Section 13A of the Pension Funds Act and financially distressed employers and employees

The Communication was issued on 26 March 2020 and it deals with the impact of Covid-19 on employers and employees and their ability to comply with the full and/or any payment of contributions in terms of section 13A. Boards of Management do not have any discretion in the application of Section 13A. Contributions that are not paid or paid late, for whatever reason, must be reported to the FSCA and late payment penalty interest is due.

Should employers find themselves in a situation where they are not able to pay full contributions to a fund, boards are required to consider the situation and apply their applicable rules in respect of temporary absence and/or reduction of contributions to ease the financial challenges. Funds without the relevant rules must submit such rule amendments urgently.

There are two possible scenarios:

Scenario 1: Members not working for a certain period and are on unpaid/partially paid leave (typically during the national lockdown, but the period may be longer depending on the employer’s operation), the temporary absence rule will apply.

Scenario 2: Members who are working, but the employer needs to suspend or reduce contributions for a period due to operational circumstances, the employer must negotiate this with the members and make an application to the fund. A rule amendment making provision for a period of reduced contributions or suspension of contributions will have to be made and submitted to the FSCA.

In the event of reduced working hours and/or reduced salaries, the rules may make provision for reduced pensionable salaries and consideration must be given to the salaries on which risk benefits are based.

Funds must attempt to ensure that full risk benefit premiums continue to be paid in order to ensure that the fund risk benefits will continue to be provided.

Any rule amendments must specify the effective date and no retrospective amendments will be allowed.

Funds must keep a proper record of the affected members and must be able to provide it to the FSCA upon request. Funds must further inform affected members of those employers’ requests to reduce or suspend contributions within 30 days of such decision. All rule amendments must be accompanied by the communication sent to members.

FSCA Communication 12 of 2020 – Impact of Covid-19: Expectations on regulated entities

The Communication was issued on 30 March 2020 and it sets out the FSCA’s expectation from regulated entities.

The FSCA emphasises that regulated entities should bear in mind the current situation and assist their customers with even more empathy, flexibility and understanding during these difficult times.

Entities must ensure that all customers are treated fairly.

Boards of management should keep abreast of risks that Covid-19 brings to their funds and take necessary steps to mitigate such risks. Funds are also encouraged to communicate Covid-19 developments and risk management strategies to members, to promote calm and minimise the risk of premature fund withdrawals.

SARS

SARS Interpretation Note 99 – Unclaimed Benefits

SARS issued Interpretation Note 99 on 30 March 2020. The purpose of the Note is to explain the treatment of lump sum benefits classified as unclaimed benefits that accrued to members both before and from 1 March 2009 for income tax purposes. Historically the legislation did not regulate when and how a lump sum benefit should be classified as an “unclaimed benefit” and as a result, fund administrators applied different rules to determine when a lump sum benefit was classified as an “unclaimed benefit”. The insertion of the definition of “unclaimed benefit” into the Pension Funds Act in 2008 introduced a period of 24 months before a lump sum benefit is classified as an unclaimed benefit.

The tax accrual regime changed in respect of withdrawal benefits in 2009 and in respect of retirement benefits in 2015 to provide that a benefit will only accrue to a member for tax purposes when he or she elects to receive the benefit. Before those dates, lump sum benefits accrued to a member for tax purposes on the date that he or she became entitled to claim the benefit.

Before 2009, in many instances fund administrators applied for a tax directive for an unclaimed benefit only when the member or the member’s beneficiaries claimed the unclaimed benefit, as opposed to when the lump sum benefit accrued for tax purposes.

In 2003, SARS requested all funds to submit a list of all lump sum benefits not claimed within a reasonable period in order to tax these unclaimed benefits.

The note explains with examples the different steps to be followed when the unclaimed benefit is paid to the member or transferred to an unclaimed benefits fund and distinguishes between if the unclaimed benefit was taxed during the 2003-project, if the unclaimed benefit that accrued after the 2003-project was taxed and if the unclaimed benefit that accrued after the 2003-project was not taxed.

It also highlights the fact that a member who claims a benefit, classified as an “unclaimed benefit”, which accrued before 1 March 2009, cannot elect to transfer the benefit to another fund. A member who comes forward after a benefit was classified as an “unclaimed benefit” and transferred to an unclaimed benefit preservation fund, after 1 March 2009, can choose to transfer that benefit to another fund.

The note therefore highlights the fact that the tax treatment of a lump sum benefit, classified as an “unclaimed benefit”, depends on the date on which the benefit accrued to the member and fund administrators should deal with unclaimed benefits as indicated by SARS.

SARS Interpretation Note 113 – Apportionment of surplus and minimum benefit requirements

The South African Revenue Service (SARS) issued Interpretation Note 113 on 3 March 2020. The note deals with the tax treatment of the actuarial surplus allocations or distributions made to members, former members, existing pensioners and employers by funds under the provisions of sections 15B, 15C, 15D or 15E of the Pension Funds Act. It also deals with the taxation of recalculation of benefits. The Interpretation Note replaces General Note 29 and Addendum A thereto, which previously dealt with this aspect.

To follow is a short summary of the noteworthy issues and the note should be consulted for a more detailed discussion of the issues:

Any lump sum benefit payable to a former member or retired member of a fund as a result of the approval of a surplus apportionment scheme under section 15Bof the Pension Funds Act (past surplus) on or after1 January 2006, is not included in the member’s gross income and is as a result not subject to tax.

Any section 15B surplus amount allocated to an active member of a fund before 1 January 2006 is used to enhance the member’s fund credit and is taxable whenhe/she becomes entitled to any lump sum benefit or annuity on exit from the fund as a result of retirement, withdrawal or death.

Any future surplus amounts allocated to an active member of a fund may only be used to enhance such a member’s share in that fund. These amounts form part of the member’s lump sum benefit or annuity payable on exit from the fund because of retirement, withdrawal or death.

Any future surplus amounts payable on or after 1 March 2009 to former members or pensioners as a lump sum are regarded as retirement fund lump sum withdrawal benefits under the new accrual provisions and are subject to the tax table applicable to retirement fund lump sum withdrawal benefits. Any after-tax amount transferred to a pension fund, provident fund or a retirement annuity fund qualifies as a member contributes to the transferee fund. Preservation funds cannot accept contributions from members and these amounts can therefore not be transferred to preservation funds.

Any future surplus amounts payable on or after 1 March 2009 to the beneficiaries of a member who hasdied before the distribution of the surplus, are regardedas retirement fund lump sum withdrawal benefits under the new accrual provisions, and are subject to the taxtable applicable to retirement fund lump sum withdrawalbenefits.

Additional amounts payable to former members as aresult of under-payments are not payment of a surplus.The additional amount must follow the member’s initialexit event. In respect of retirement benefits of a pension fund, the retired member will only be entitled to take 1/3of the total benefit (i.e original benefit plus the additionalamount) in cash. The balance may be transferred to theannuity provider. Should the annuity provider not be in aposition to accept the lump sum, the additional amountis payable as a once-off bonus taxable as income.

In respect of retirement benefits of a provident fund, the former member will be able to receive the additional amount as a lump sum benefit.

General

FSCA Interpretation Ruling 1 of 2020 – Application of section 37C of the Pension Funds Act to paid-up members and deferred retirees

The FSCA issued the interpretation ruling with the accompanying Communication 10 of 2020 on 25 March 2020 with the intention of providing clarity, consistency and certainty in the interpretation and application of section 37C of the Act.

According to the ruling, a paid-up member, deferred retiree and a member of an unclaimed benefit fund is a “member” as defined in the Act and section 37C is therefore applicable on the death of these members.

Section 37C will however not apply where the member had already provided the fund with a written instruction to pay out or transfer the benefit prior to the member’s death.

In terms of the communication, funds may now finalise their rules to reflect the view in the interpretation ruling.

The FSCA will engage with National Treasury and all key stakeholders to make amendments to the relevant sections of the Act to expressly clarify the application of section 37C to paid-up members and deferred retirees.

Lawyers still argue that the Act is not clear on this issue and that the FSCA does not have the power to use an interpretation ruling to effect a change which should be a matter for the legislator. The argument is that the Interpretation Ruling is not binding on third parties, and more specifically on the executor of a deceased member’s estate.

It is uncertain what a court will find if a fund pays the benefit in respect of a deceased paid-up member or deferred retiree in terms of section 37C, and the executor of the member’s estate subsequently claims that the benefit should have been paid to the estate. However, in our view, the risk of paying in terms of section 37C will be minimal if the executor of the estate is notified early in the process that the benefit will be paid in terms of section 37C and confirms that he/she is comfortable with this.

FSCA Communication 6 of 2020 – Exemption of large funds from certain prescribed formats for preparing financial statements

Communication 6 of 2020 with the accompanying FSCA Notice 5 of 2020 was issued on 5 March 2020.

The FSCA intends to issue a new prudential standard to prescribe the format of financial statements pertaining to large funds (those with total assets exceeding R50 million). The prudential standard will incorporate the illustrative auditor’s reports approved by the Independent Regulatory Board for Auditors (IRBA).

The FSCA is, as an interim measure, exempting large funds from using the current prescribed schedule D (independent auditors report) and IB1 (independent auditors report on compliance with regulation 28) in the current Board Notice 77 of 2014 on the condition that the IRBA’s illustrative auditor’s reports are used.

The exemption will apply retrospectively from 1 March 2018 until the intended prudential standard has been issued.

FSCA Communication 7 of 2019 – The role and independence of the Principal Officer

The FSCA published Communication 7 of 2019 on 12 December 2019. The communication addresses Directive 8 of 2018, which deals with the prohibition of gratification.

According to the FSCA, the simultaneous employment of the principal officer by a service provider is impermissible and is also undesirable. The FSCA intends to write to those funds that have been identified to take remedial actions in order to bring the fund into compliance. The FSCA is proposing a maximum period of six months within which to regularise the appointment of a new principal officer.

There are ongoing discussions in the industry regarding the communication and the FSCA’s approach.

FSCA Communication 7 of 2020 – Terminating funds with historically outstanding actuarial valuation reports and annual financial statements

Communication 7 of 2020, with the accompanying FSCA Notice 6 of 2020, was issued on 6 March 2020.

The Communication sets out a process which may be followed by funds that have no remaining members but have historical outstanding actuarial valuation report submissions and outstanding annual financial statements.

A fund may combine statutory submission reports for several reporting periods into a single report, subject to the following conditions:

- The fund’s surplus apportionment scheme has been approved, or a nil return has been noted, or the fund commenced after 7 March 2002;

- No remaining active members, paid-up members/deferred members or pensioner as at 31 December 2019;

- The fund has effected a section 14 (1) or section 14 (8)transfer and the assets matching the transfer have been transferred out;

- The fund is pending deregistration following section14 transfers or the liquidator’s appointment has been approved;

- There is no pending litigation by or against the fund; and

- The net assets of the fund (investment portfolios plus bank account assets less unclaimed benefits) as at31 December 2019 were below R250 000.

The authorized representative of the administrator, valuator, board, and the principal officer of the fund must certify that the fund complies with all the above conditions.

On approval of the consolidated valuation report, an exemption for a further three-year period will be granted to allow time to proceed with the deregistration process. The fund will then be expected to submit outstanding financial statements within 3 months and apply for deregistration within 6 months of approval of the valuation report.

Where a liquidator has been appointed to distribute the remaining assets in the fund, the consolidated financial statements should be until the date on which the appointment of a liquidator was approved.

Funds must approach the FSCA before 30 June 2020, to commit to an action plan in this regard. All submissions of consolidated valuation reports and financial statements must be made prior to 30 April 2021.

Survey

Survey on sustainable finance practices in retirement funds

The FSCA has requested boards of management and principal officers of retirement funds to complete a voluntary survey on sustainable finance practices by 31 May 2020. The FSCA stated that the survey is not linked to prescribed assets. The motivation is driven by rapidly evolving global trends towards green and sustainable finance and ensuring that South Africa can leverage these opportunities while reinforcing financial stability through good Environmental, Social and Governance (ESG) practices.

The survey aims to capture the current practices as well as obstacles related to sustainable finance among South African retirement funds.

Responses will help ensure that future reporting requests keep pace with the realities of retirement fund investment processes. A summary will be provided to those completing the survey to assist in future with reporting in line with the ESG requirements of Regulation 28.