Economic Commentary – Review of Q1/2024

The economy

We started 2024 with the greatest of expectations. Inflation was finally under control and economists projected as many as three or four domestic interest rate cuts of 0.25% in 2024. When interest rates are cut aggressively, mainstream economic growth accelerates and the prices of financial assets improve rapidly. The expectation was that lower inflation and lower interest rates would contribute to better economic growth.

The World Bank projected that the global economy would expand by 2.4% in 2024 (3.1% in 2023) while the South African (SA) economy was projected to expand by 1.0% this year (0.6% in 2023).

The rand exchange rate will likely remain weakish initially but strengthen later in the year when the expected interest rate cuts commence.

Unemployment remains a major concern in the domestic economy at more than 32%, with youth unemployment approaching two-thirds of school leavers and new graduates.

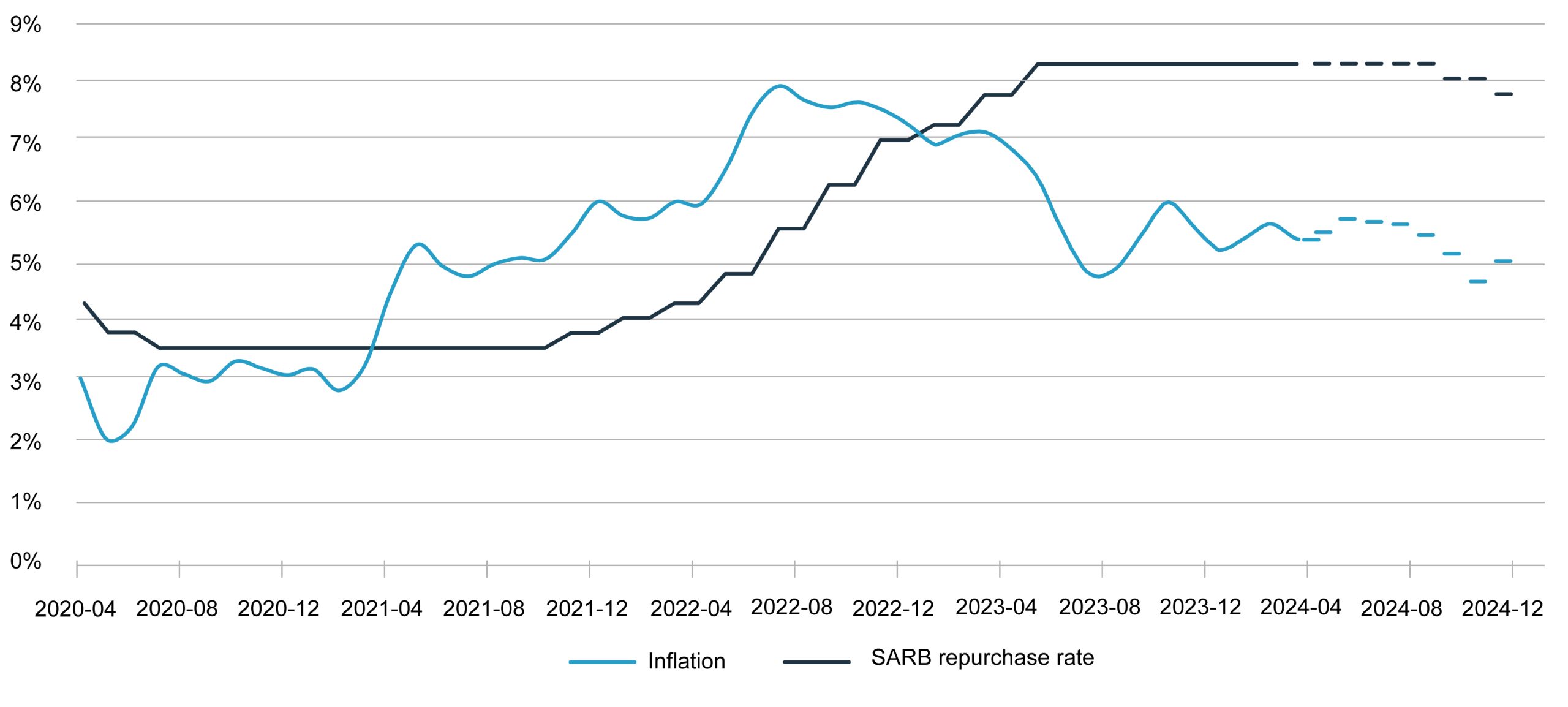

Towards the end of March 2024, it became evident that the SA inflation rate is not likely to be 5.0% for 2024, but closer to 5.3%. The upward revision takes account of significant contributions to inflation by electricity, fuel and food prices.

The oil price increased by 9% over the 12-month period and by 13% for the quarter ended March 2024. Inflation on electricity is currently running at 15%. The rand exchange rate weakened by 4.7% over the 12-month period and by 2.0% for the quarter to 31 March 2024.

The Department of Agriculture’s Crop Estimate Committee released its final 2024 estimate for the summer rainfall area of South Africa. The final crop estimate reveals that the maize crop is expected to be 13.3 million tonnes in 2024 compared with the 16.4 million tonnes harvested in 2023. As a result, the Near White Maize Future listed on SAFEX rose to R5 350 a tonne on 31 March 2024 compared with the R4 006 per tonne on 31 December 2023.

Graph: Domestic consumer price inflation and SARB’s repurchase rate

{kind=link}

Financial markets

| % Change March 2024 | Most recent quarter | Calendar

YTD |

1 year

(p.a.) |

3 years (p.a.) | 5 years (p.a.) | 10 years (p.a.) |

| All Share Index | -2.2% | -2.2% | 1.5% | 8.1% | 9.7% | 8.1% |

| Listed Property | 3.8% | 3.8% | 20.5% | 13.9% | 0.7% | 3.1% |

| STeFI Composite | 2.1% | 2.1% | 8.4% | 6.1% | 6.0% | 6.5% |

| ALBI | -1.8% | -1.8% | 4.2% | 7.4% | 7.0% | 7.7% |

| MSCI All Country World ZAR | 10.2% | 10.2% | 29.9% | 16.2% | 17.2% | 15.7% |

| Bloomberg Global Aggr. Bond ZAR | -0.7% | -0.7% | 4.8% | 2.8% | 3.8% | 5.8% |

| Rand (+ stronger, – weaker) | -2.0% | -2.0% | -4.7% | -6.9% | -4.5% | -4.4% |

| Inflation | 1.9% | 1.9% | 5.3% | 6.5% | 5.7% | 6.4% |

| Gold ZAR | 10.4% | 10.4% | 18.6% | 18.7% | 17.4% | 11.9% |

Major domestic financial markets continued to post single-digit returns for the 12 months ended March 2024.

The exception is listed property, which achieved a return of 20.5% for the 12-month period. Individual counters in the listed property environment provided a diverse range of returns with some counters returning more than 20% for the 12-month period, but some of the stalwart counters struggled to deliver positive performance.

Domestic bonds performed poorly in the first quarter of 2024 (-1.8%) and the annual contribution is disappointing at 4.2%.

The poor investment return on domestic shares reflects the unexciting performance of the local and global economies. Commodity stocks performed poorly for the 12 months, but recovered in the recent quarter, while financials performed better over the 12 months to March 2024, but poorly for the quarter to the same date.

Gold continued to yield exciting results. The gold price rose 18.6% over the 12-month period to 31 March 2024. It appears that the demand for gold could be coming from central banks that are in the process of diversifying monetary reserve holdings.

Graph: Gold Price – USD per Troy Ounce

{kind=link}

We remain cautiously optimistic about the potential performance of financial markets over the next 12 months, despite the poor performance of the domestic economy expected in 2024.

Information for this article has been obtained from several sources: National Treasury, South African Reserve Bank, Stats SA and IRESS.