Economic Commentary – Review of Q2/2023

The economy

The major themes that impacted our environment in the second quarter of 2023 were geopolitics and the rand.

Even though South Africa is only a regional geopolitical power, several issues pushed geopolitics to the top of the national agenda:

- In December 2022, a sanctioned Russian cargo ship docked at the Simon’s Town naval harbour to unload military cargo in fulfilment of a pre-Covid order from Russia. The event caused a commotion, as civilian observers noted both night-time unloading and reloading activities.

- Following the docking of the Lady R in Simon’s Town, the South African Navy conducted joint naval exercises with Russia and China in the southern Indian Ocean in February 2023.

- In May 2023, the US Ambassador to South Africa, Mr Reuben Brigety, accused South Africa of shipping armament to Russia despite sanctions imposed against Russia by the US, the EU and allies. South Africa has not imposed sanctions against Russia.

- Shortly thereafter, host country Japan made it clear that South Africa was not invited to the G7 Hiroshima Summit in May 2023. Until then, South Africa had been invited regularly to the annual G7 summits as an observer representing Africa. Japan’s government stated it believed South Africa could no longer speak for the continent on international affairs.

- Throughout the period, South Africa continued to reach out to Russia with several government ministers and high-ranking officials visiting Russia.

- South Africa is scheduled to host the annual BRICS Summit in Sandton in August 2023, when the heads of state of Brazil, Russia, India, China, and South Africa will meet to discuss matters of mutual interest. The International Criminal Court (ICC) previously issued a warrant of arrest for Russian President Vladimir Putin. South Africa is a member of the ICC and a signatory to the Rome Statute. The Rome Statute establishes the ICC’s jurisdiction over the 15 forms of crime against humanity including offences such as murder, rape, imprisonment, enforced disappearances, enslavement (particularly of women and children), sexual slavery, torture, apartheid, and deportation in its 123 member countries. As a member country, South Africa is obliged to arrest President Putin if he visits South Africa for the BRICS Summit. To arrest a sitting head of state would place South Africa in an untenable position.

- To influence Pretoria, indications emanating from Washington are that South Africa may be excluded from the US African Growth and Opportunity Act (AGOA), which allows certain listed African countries to have preferential trade access to the US and may even be subjected to secondary sanctions. Secondary sanctions are targeted sanctions against specific corporates or individuals in target countries.

- At the same time, a host of heads of state and government ministers from Europe are visiting South Africa to express concern and to solidify relationships with South Africa.

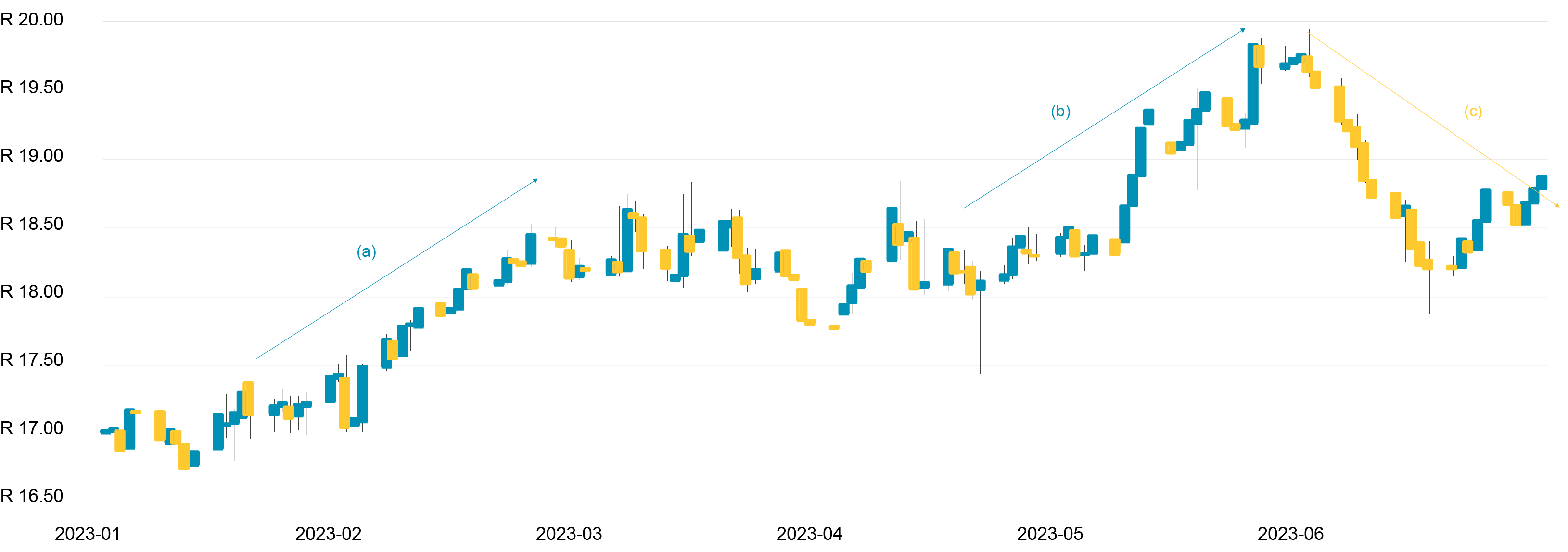

Around February 2023, the rand/US dollar exchange rate weakened from R17.00 to R18.50, mainly because of sales of domestic shares and bonds by non-residents who then repatriated their funds to their home countries (marked “a” on chart 1). In May 2023, the exchange rate weakened further, from R18.25 to R19.80, mainly because of the geopolitical developments involving South Africa (marked “b” on the chart). Notably, as soon as the temperature in the political environment dropped, the exchange rate strengthened from R19.80 to R18.10 in June 2023 (marked “c” on the chart). At quarter-end, the rand traded weaker again, at a level of approximately R18.70.

Chart 1 – Rand/US dollar exchange rate

{kind=link}

The South African economy is facing headwinds, as mining production and industrial manufacturing have been trending downwards for decades now. Fuel refining capacity is lower than previously, and gross fixed capital investment is at a low level. Calendar 2023 has so far seen record levels of rolling blackouts, which has a negative impact on South Africa’s economic growth potential. Inflation remains elevated, and some economists believe we are close to the top of the interest rate cycle while others believe interest rates are likely to continue rising in the next six months. Either way, interest rates are likely to remain high for the remainder of the year. Households and consumers are under pressure, and both business and consumer confidence are languishing at concerning levels. Government finances remain a concern, as fiscal discipline slips and South Africa’s debt-to-GDP ratio reaches a worrying level. South Africa faces the possibility of higher taxes as Government forges ahead with the implementation of costly policies such as the National Health Insurance scheme.

Yet, despite all the challenges, the South African economy remains remarkably resilient.

The economy expanded by 0.4% quarter on quarter to the end of March 2023, and inflation is down to 6.3% as at end of May 2023. The balance on the current account had swung into deficit by December 2022 (-3.8% of GDP), but the deficit improved in the first quarter of 2023 (-1.4%).

Reports indicate that, according to recent estimates by Eskom, rooftop photovoltaic solar installations added capacity of as much as 4 000 MW and wind-powered installations added more than 2 000 MW. A further 6 000 MW is expected to be brought onstream in 2024. In addition, the interest rate cycle is expected to turn in 2024, as inflation is brought under control and the global economy is expected to expand.

The global economy is expected to grow faster in 2024 than in 2023. With some of the more severe challenges out of the way in South Africa, the growth rate for the South African economy may be as high as 1.8% in 2024, in contrast to the projected 0.1% for 2023.

Financial markets

In the City of London, the adage “Sell in May and go away; don’t come back until St Leger’s Day” warns speculators in the city to sell their shares ahead of the Northern Hemisphere summer holidays, before buying them back in autumn. (St Leger’s Day refers to an annual horse race run in Doncaster, York in September.)

2023 may well be a year in which the adage proves to be correct. The FTSE/JSE All Share Index TR is up 0.7% for the quarter, resources shares are down 6.4%, financial shares rose 6.0% and industrial shares gained 3.7% for the quarter. Listed property shares rose 0.7% for the quarter while inflation-linked bonds (real cost of capital) increased from 4.05% at the end of March 2023 to 4.43% at the end of June 2023. Measured in US dollars, global shares are up 7.5% for the quarter, but in rand terms, these shares gained 13.9% over this period.

Gold shares posted attractive returns for the quarter while bank shares capitalised on renewed interest, and on the industrial board, Woolworths, Reinet and CF Richemont performed well. Impala Platinum, Sun International, Tiger Brands and AB InBev all struggled. On the JSE’s main board, 46% of shares closed the quarter higher and 54% ended lower.

Interest-bearing investments also showed lacklustre performance as domestic bonds lost 1.5% over the quarter. The money market improved by 1.9% for the quarter. Nominal bonds with maturity dates longer than 12 years softened by 2.6% and inflation-linked bonds of the same maturity weakened by 2.5% over the quarter. Offshore bonds were 1.5% softer for the quarter when measured in US dollars, but 4.3% up when measured in rands.

The rand was especially volatile over the quarter opening at R17.79 but weakening to close May 2023 at R19.73 (the weakest intra-day trading saw the rand exchange rate touch R20 on 30 May 2023). Subsequently, the rand strengthened to the mid-R18 level (strengthening to R17.86 on 16 June 2023 during intra-day trading). The rand closed the quarter at R18.85, thus weakening by only 5.6% over the quarter despite the volatility.

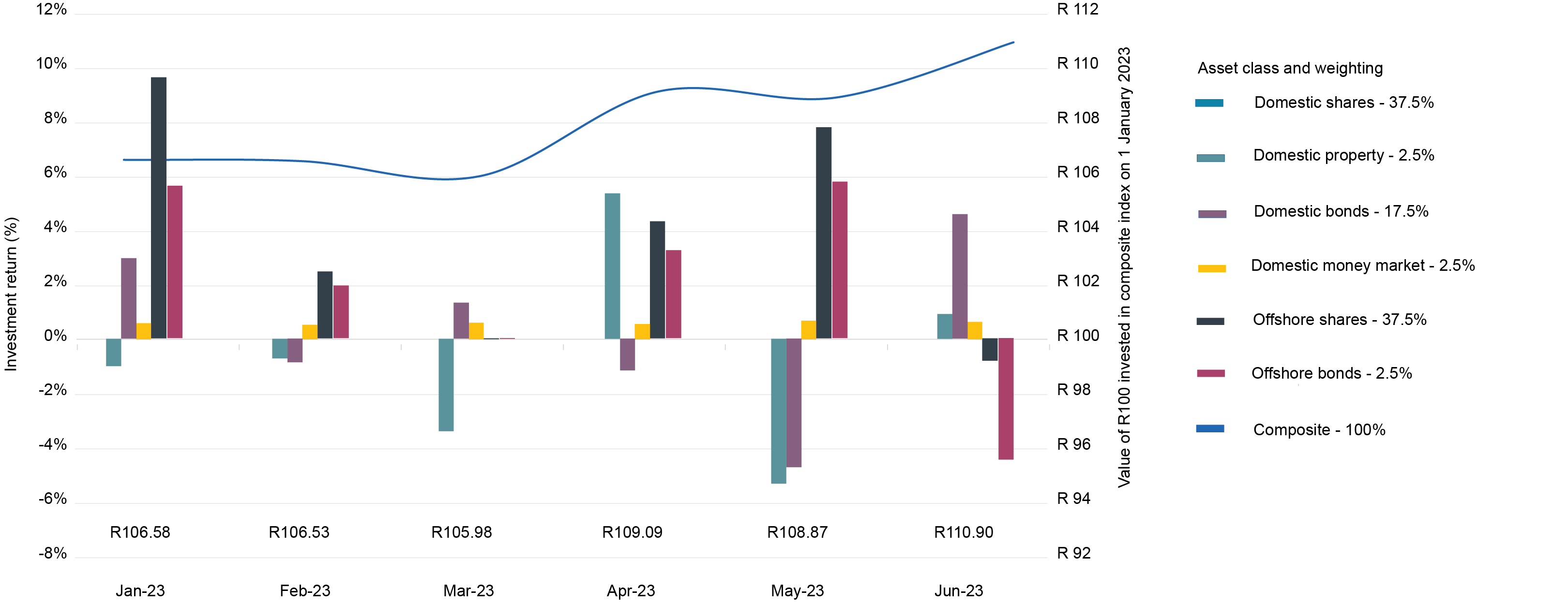

The investment returns generated by the indices representing the asset classes in which South African retirement funds typically invest are as follows:

| % Change June 2023 | Most recent quarter | Calendar YTD | 1 year

(p.a.) |

3 years (p.a.) | 5 years (p.a.) |

| All Share Index | 0.7% | 5.9% | 19.6% | 18.9% | 11.6% |

| Listed Property | 0.7% | -4.4% | 10.0% | 12.7% | -3.3% |

| STeFI Composite | 1.9% | 3.7% | 6.8% | 5.2% | 6.5% |

| BEASSA ALBI | -1.5% | 1.8% | 8.2% | 8.2% | 8.6% |

| MSCI All Country World ZAR | 13.9% | 26.5% | 35.5% | 14.6% | 15.7% |

| Barclays Global Aggregate ZAR | 4.3% | 12.3% | 14.2% | -2.3% | 5.4% |

| Rand (+ strengthening, – weakening) | -5.6% | -9.7% | -13.6% | -2.6% | -5.4% |

| Inflation (estimate) | 1.1% | 2.8% | 5.8% | 6.4% | 5.5% |

| Gold ZAR | 2.2% | 15.6% | 21.4% | 5.3% | 15.9% |

The investment return on a Regulation 28 compliant super-aggressive index composite with maximum offshore exposure and exposure to shares came to 11.3% for H1 of 2023. Early indications are that global balanced funds achieved returns of about 8% for the quarter.

Chart 2 – Value of R100 invested in composite index on 1 January 2023

{kind=link}

Long-term investment returns have not recovered sufficiently after several years of elevated volatility, for members to be comfortable.

Information for this article has been obtained from several sources: National Treasury, Stats SA and IRESS.