How long does it take to bring inflation to heel? – 15 May 2023

An economic analysis

Inflation cycles are not all the same.

Conventional economic literature contends that inflation is a sign of an overheating economy. It occurs when demand for goods and services outstrips the supply of these goods and services, which leads to higher prices (inflation).

Monetary authorities effectively control rising inflation by raising interest rates. Having to pay higher debt servicing cost reduces discretionary household expenditure and dampens aggregate demand in the economy. With the demand for goods and services under pressure, the supply of these goods and services decreases, bringing about lower prices as the economy cools or even contracts. Similarly, when monetary authorities wish to stimulate economic growth interest rates are reduced, resulting in increased discretionary household expenditure, which in turn leads to expanding demand for goods and services.

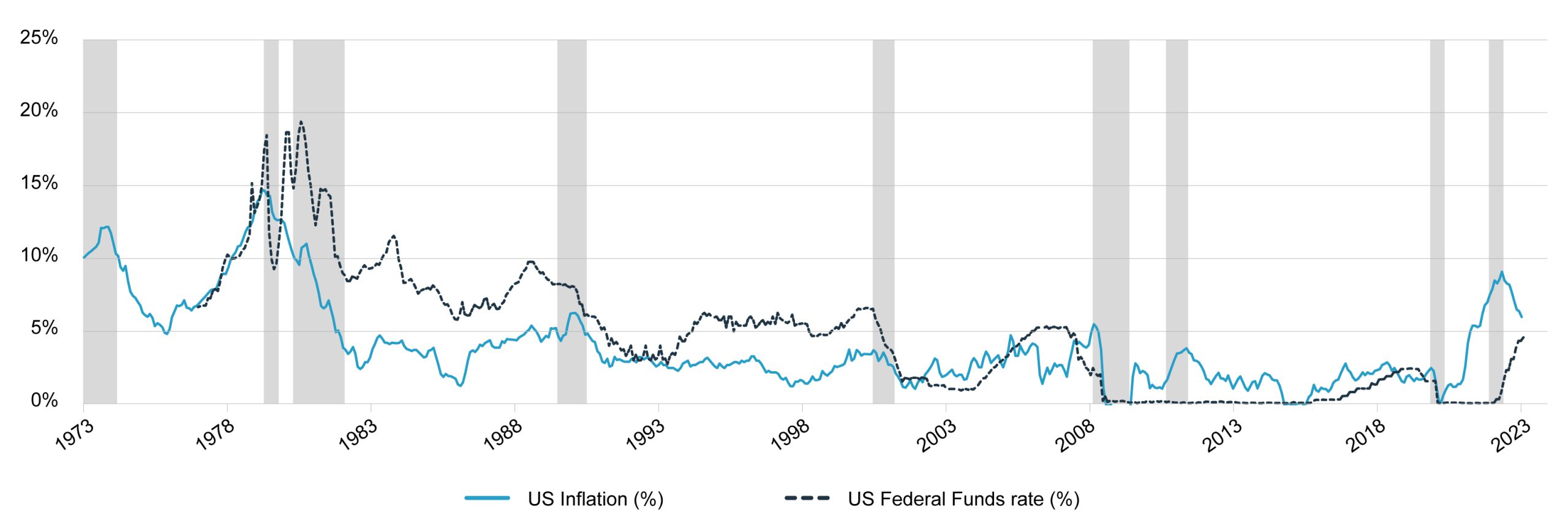

Click here to view graph: US inflation and policy interest rates and periods of economic contraction

{kind=link}

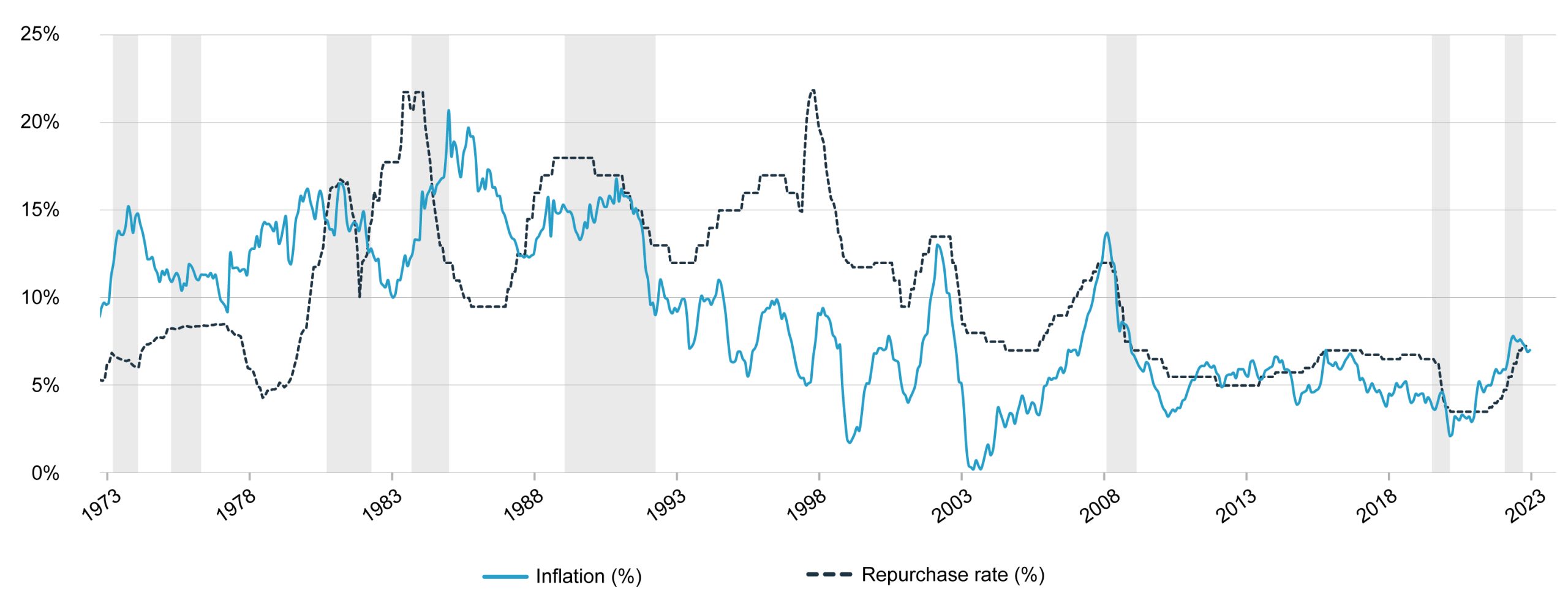

Click here to view graph: South African inflation and policy interest rates and periods of economic contraction

{kind=link}

We differentiate between three types of inflation:

- Demand-pull inflation (i.e. when an economy overheats)

- Cost-push inflation (i.e. is when the price of input cost rises unrelated to demand, e.g. the oil price shock in the 1970s)

- Inflation resulting from rising administered prices (e.g. rising municipal tariffs stemming from charges related to higher property valuations and rising electricity prices in South Africa).

Demand-pull inflation was evident in the late 1980s and again in the period leading to 2008. Cost-push inflation prevailed in the 1970s and 80s because of harsh increases in the oil price and production cuts by OPEC producers; and has surfaced again since 2020, because of global supply constraints following the lockdowns implemented to contain the Covid pandemic.

Raising interest rates is effective to control demand-pull inflation, and a callous but nevertheless effective way to control cost-push inflation or inflation that results from rising administered prices. It is believed that demand-pull inflation almost immediately reacts to rising interest rates, as it has a direct impact on discretionary household expenditure, but less so with cost-push inflation. When cost-push inflation prevails and interest rates are raised, discretionary household expenditure comes under pressure but the cost-push factors don’t necessarily experience the same pressure. For example, higher interest rates did not contain rising petrol prices during the oil crises in the 1970s, nor did they dampen rising food prices stemming from Russia’s invasion of Ukraine and the current electricity crisis. Households resort to cutting back on other discretionary expenditure items as patterns shift to balance household budgets.

Our analysis shows that it takes approximately 18 months to get inflation under control after interest rates have been raised. Inflation normally responds within six months of interest rates peaking. Inflation has started to come down in 2023, but interest rates are still increasing, suggesting that the present bout of inflation presents a tougher challenge.

To date, the South African Reserve Bank’s Monetary Policy Committee has increased the repurchase rate on nine separate occasions and by a total of 4.25% in its attempt to bring inflation to heel. We expect the SARB to continue with its rate hiking policy until it is evident that inflation is under control. SARB Governor Kganyago correctly pointed out that “inflation is essentially a regressive tax – a tax which impoverishes those whom society should really be helping”.

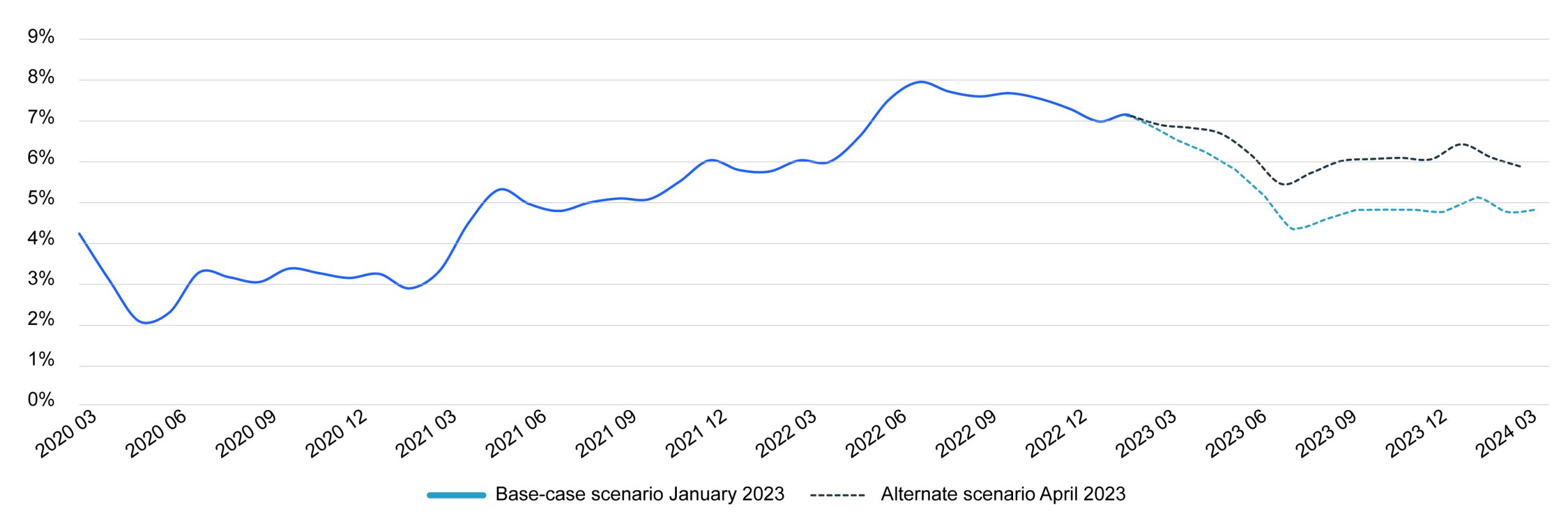

In our analysis and review of economic factors in January 2023, we stated our belief that the consumer price inflation rate would come down in 2023 to reach an average of 5.6% for the year and an average of 4.7% in 2024.

Subsequent developments suggested that inflation is more viscous than believed previously. There are five inflationary concerns in 2023:

- Fuel prices (impacted by both the oil price and the rand)

- Food prices (driven by bread prices and chicken prices etc.)

- Salary increases

- Availability of electricity (load shedding)

- Electricity prices (an increase of more than 20% is expected later in the year).

On the positive side, the technical base effect contributes to the possibility of lower inflation in 2023. The base effect means that the percentage price increases should slow in 2023, because the price increases are being calculated off a higher base in 2022. The base effect should be significant in the coming months (April to July 2023), because inflation increased sharply during the corresponding period in 2022 (from 5.9% to 7.8%).

At this stage, we believe it to be prudent to add a second scenario that downplays the reducing impact of the base effect on inflation over the next four months. Should inflation remain higher because of fuel prices, food prices, the (un)availability and price of electricity and salary increases, the average inflation rate for 2023 could be 6.2% (as shown in the chart below).

Click here to view chart: South African Consumer Price Inflation projections for 2023

{kind=link}

Inflation projections for the next 12 months are central to our asset class return expectations. The second scenario represents a departure from our base-case scenario and suggests that our asset class return scenarios could perhaps be more muted than expected if inflation remains higher than originally expected.

Whichever way one looks at the situation, the next four months will be crucial for inflation, and we expect inflation to become benign only towards 2024.

Information sourced from: Information sourced from: National Treasury Budget 2023-24 and IRESS