Where will financial markets take investors in 2023? – 10 February 2023

Investors will remember 2022 as a particularly difficult year in financial markets. For only the third time in a century, both equities and bonds posted negative returns in the United States (US). The fundamental tenet of risk diversification did not hold true in 2022, as fixed income investments provided neither income nor risk diversification when equity prices dropped by 20%.

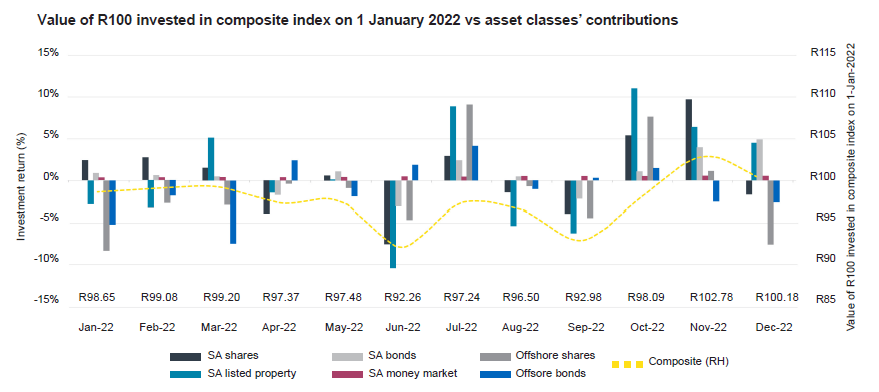

South African (SA) financial markets performed better than their developed market counterparts in 2022. The FTSE/JSE All Share Index posted 3.6% (including dividends) and the BEASSA All Bond Index achieved 4.3%. Local investment returns were particularly strong as shares posted 15.2% and bonds 5.7% in the fourth quarter of 2022. It is fair to say that the strong recovery in SA financial markets during 4Q 2022 saved the day. By the end of the third quarter, the All Share Index was down 10.1% for the year to date while the All Bond Index was down 1.3% for the same period.

Graph – Value of R100 invested in composite index on 1 January 2022 vs asset classes’ contribution

{kind=link}

Will 2023 be more kind to investors than 2022?

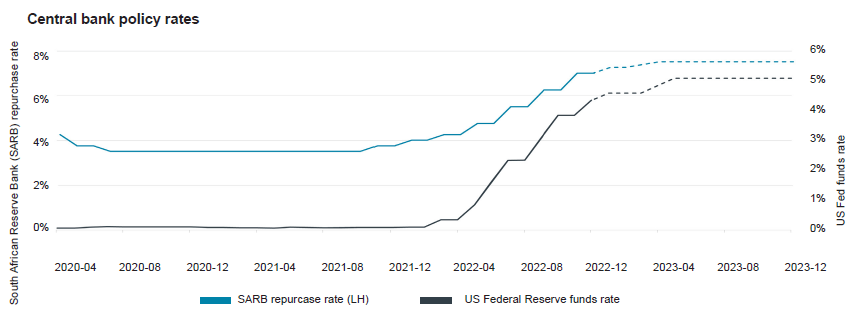

Developed economies are widely expected to enter economic recessions in 2023 because of elevated interest rates, which have been raised to combat higher inflation. Higher interest rates act to dampen demand for goods and services in economies. Europe is likely to bear the brunt. Even though recessions are looming, central banks are expected to continue hiking interest rates in early 2023, because they believe high inflation is a bigger problem for economies than recessions. The base case view is that the US Federal Reserve Board (the Fed) will implement two hikes of 0.25% each before pausing to maintain interest rates for the duration of 2023.

Global inflation is expected to come down in 2023, but perhaps not as quickly or by as much as anticipated initially. The current inflation experience was fuelled by central banks around the world lowering interest rates to unsustainable levels in 2020 and 2021 and holding rates low for too long. Supply constraints in the labour market as well as the goods market (e.g. the extended Covid lockdowns in China, the war in Ukraine and the expenditure shift away from services to goods during the lockdowns) have added to the inflation problem. Going forward, the average inflation rate may well be much higher than the inflation average experienced over the last two decades.

South Africa’s inflation is expected to fall sharply in 2023. Recently, inflation was driven by higher fuel prices and higher food prices. The price of fuel has already come down because of the lower oil price and the improved rand/US dollar exchange rate. Likewise, food inflation – to some extent driven by higher fuel prices – should follow suit. It must be noted that the food price index in South Africa is not correlated with the UN FAO’s food price index (r2 = 0.06) but shows remarkable correlation with the fuel price index (r2 = 0.91). As fuel inflation recedes, so lower food inflation should follow in South Africa.

Financial markets are forward-looking and discount expectations of future developments. The elevated interest rates and probability of economic recessions contributed to the headwinds experienced in financial markets in 2022. The consensus view is that inflation will edge down in 2023 and that further interest rate increases beyond the initial increases in the first half of 2023 are unlikely. However, we need to see how actual experience unfolds. Assuming that inflation becomes less of a concern, financial market participants will likely see interest rate reductions in 2024 (some even expect the first interest rate cut late in 2023). Looking forward and discounting expectations of future developments, 2023 could likely see pleasing investment results, as long as inflation behaves itself.

Graph – Central bank policy rates

{kind=link}

After experiencing recessions in 2023, developed economies are expected to recover by 2024. Recession-driven weaker corporate earnings have been discounted by share prices already. The central question is how much of the anticipated damage to earnings has been priced in. Investors are looking for the opportunity to expand their equity exposure. If recession-driven damage to corporate earnings has been discounted sufficiently, developed equity markets currently provide investors with good entry levels. If not priced in sufficiently, it means developed financial markets could continue to provide modest outcomes. The currently good long-term entry point to invest in developed market equities may become even more favourable if earnings are more severely impacted by the recession.

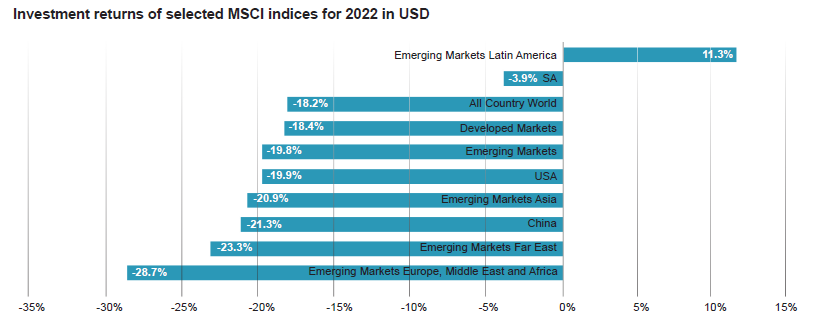

Emerging market shares present investors with more attractive opportunities, but emerging markets are not homogenous. For example, Latin American share prices were not affected by the downturn in 2022 (Argentina delivered +33.5%, Brazil +14.7% and Colombia +21.9% in US dollar terms) but will be hard pressed to generate the same returns for a second year running. Share prices in China were depressed by the country’s zero-Covid policy and other regulatory steps in 2022 but may do better in 2023 as constraints are lifted. Emerging markets in Eastern Europe performed poorly because of their proximity to the Russia/Ukraine war and dependence on Russian natural gas supplies.

Graph – Investment returns of selected MSCI indices for 2022 in USD

{kind=link}

After declining by approximately 20% during the year, local share prices recovered well to close the year down only 0.9% (but up 3.6% when dividends are included), and investors believe these shares are attractively priced. SA share prices are sensitive to developments in China, particularly Naspers, because of its exposure the Chinese internet company Tencent and commodity producers that could benefit as China lifts lockdown restrictions. It is equally possible to foresee conditions for SA shares to achieve a return of either 20% or 5% for 2023, so any return expectations are to be approached with the necessary caution. Foreign investors view SA shares with caution and seem to prefer emerging market shares from other countries.

Domestic listed property is expected to provide investors with a reasonable yield in 2023. It would require a brave heart to project a repeat of the record levels of 2017, but a double-digit return driven by income yield certainly seems possible. Such an advance would restore the listed property yield to pre-Covid levels.

Global fixed income investments provided neither income nor protection (diversification) to global investors in 2022. Bond yields in developed markets rose sharply as central banks raised interest rates aggressively to fight inflation. As inflation recedes and central banks are likely to pause interest rate hikes towards the second half of 2023, global bonds should offer attractive opportunities. Globally, high quality credit bonds are preferred over government bonds (a risk- seeking approach). Emerging market bonds (including SA bonds) are also particularly attractive.

One of the central themes that dominated financial markets in 2022 was US dollar strength. The greenback traded at $0.9557 against the euro and the US Dollar Index at 114.64 on 27 September 2022. The rand was volatile and traded at R18.40/US$ one month later. Subsequently, the US dollar has weakened, and the rand has so far strengthened into 2023. This trend is likely to continue for the remainder of 2023 impacting developments in financial markets. However, the risk of South Africa scoring “own goals” is always high and this could dampen enthusiasm for the rand. A stronger rand could impede the contribution made to investment returns by offshore exposure.

Finally, investors should consider geopolitical risks. One of the lessons learnt in 2022 is that despite the American hegemony, armed conflict overturning expectations of global financial markets remains possible. A shooting match may occur elsewhere in the world as the US and European governments did not put boots on the ground in the Russia/Ukraine war (e.g. in the Koreas, following a drone incursion from North Korea that went undetected until some drones reached Seoul, according to unconfirmed news reports). In addition to armed conflict, other geopolitical disruptions may occur, such as enhanced technology rivalry, an energy crunch, or dire consequences from the global climate change crisis.

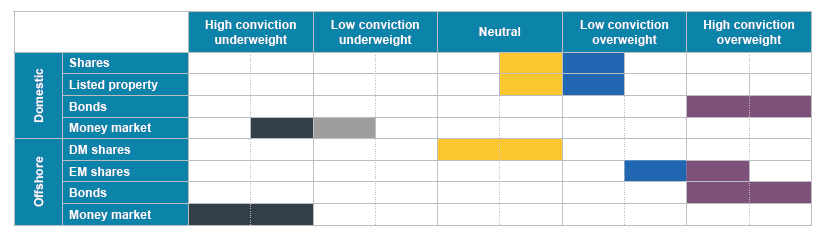

In summary, investors should consider investing in portfolios with:

- An overweight exposure to domestic bonds (high conviction position)

- An overweight position particularly in investment grade credit (high conviction position), closing out any historic underweight exposure to offshore bonds

- An overweight exposure to local listed property (high conviction position), depending on risk tolerance

- An underweight exposure to money market assets

- A flexible approach to shares:

- Domestic shares could easily generate either mediocre returns on the back of slow earnings growth or superior returns based on yet another strong contribution from commodities, tech and banking (low conviction position).

- Consider an overweight exposure to other emerging market shares (high conviction position).

- Investment managers should continuously assess developed equity markets to determine whether the potential damage of economic recessions has been discounted by share prices. If so, build up quality exposure positions; if not, maintain a careful approach to developed equity markets (low conviction position

Table – Summary of portfolios investors should consider investing with

{kind=link}

Depending on how events in financial markets unfold in 2023, investors could expect investment returns ranging from merely matching inflation to beating the long-term objective of 6% above inflation after fees.

Information sourced from: Stats SA, SARB, UN Food and Agriculture Organisation and Iress